Quick Summary

- MFIs can enhance collections and repayment discipline by digitising center visits using LMS, LOS, and Field Force Automation (FFA).

- Current manual processes lead to poor visibility and execution gaps in collections, risking portfolio health.

- Digitisation allows for real-time tracking of customer visits, ensuring accurate attendance and immediate visibility into meeting outcomes.

- Integrating LMS, LOS, and FFA creates a robust framework for MFIs, enabling better risk management and operational efficiency in center meetings.

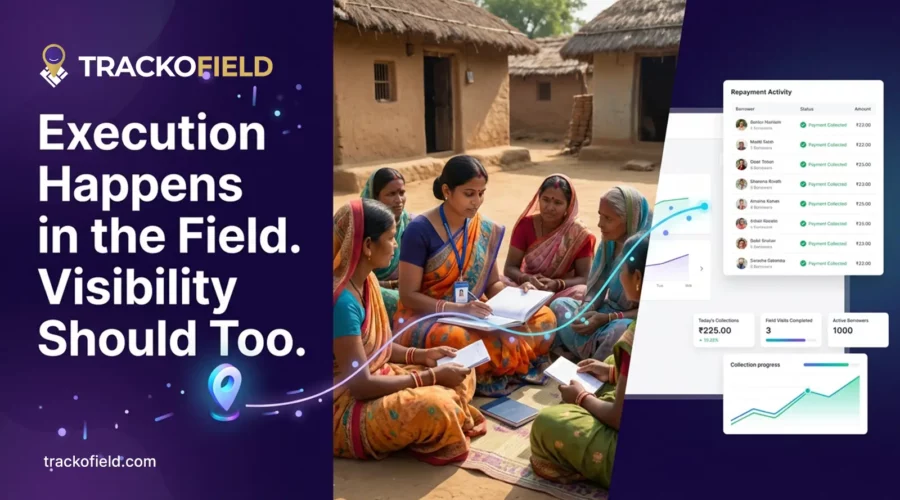

TrackoField digitises center meetings with LMS, LOS, and Field Force Automation, converting real-time field execution into verified collections data for repayment discipline and portfolio control.

Digitisation in microfinance has largely strengthened central systems. LOS, LMS, and MIS dashboards have made compliance, reporting, and portfolio tracking stronger.

Three problems persist. Poor collections. Slow visibility. Too much time lost to reconciliation.

In microfinance, execution does not happen in reports or dashboards. It happens during customer visits and center meetings.

Untracked field visits mean no system can give you real control. Collections and portfolio health are decided in the field. Not in dashboards.

MFIs must digitise center meetings and field visits. Not as an add-on. As core infrastructure.

Center Meetings Are the Core Execution Layer in MFIs

Center meetings are where microfinance operations actually unfold.

Every repayment cycle, borrower interaction, and early warning signal begins here.

During a typical center meeting:

- Customer visits take place

- Collections are made

- Attendance and repayment discipline are enforced

- Field officer execution becomes visible

- Group-level risk patterns begin to surface

When center meetings run well, portfolio performance stays stable. When they don’t, gaps emerge quietly and grow over time.

If center meetings stay manual, the data lies. What gets reported will not match what actually happened.

The Reality of Visits and Center Meetings Today

Execution Challenges in MFI Center Meetings

Yet most MFIs still run center meetings and field visits on paper or spreadsheets.

Common gaps include:

- Attendance recorded manually, with no verifiable proof of borrower or officer presence

- Collections entered after the meeting, often at the branch or end of day

- No system-level proof of repayment at the point of collection

- Dependence on post-meeting reconciliation instead of real-time checks

- Management visibility arriving days later, when corrective action is already delayed

They gaps exist because execution is not captured at the point of action. Over time, teams stop trusting the data. And by then, it is too late to act.

Why LMS or LOS Alone Cannot Fix Execution Gaps

Most MFIs already run LOS and LMS platforms. These systems are necessary but not sufficient.

Limitations of LMS

Loan Management Systems manage repayment schedules, balances, and portfolio reporting. However, they rely on inputs that are often delayed or uploaded manually. LMS platforms cannot verify if a collection actually happened. They only record what someone enters later.

Limitations of LOS

Loan Origination Systems ensure structured onboarding and policy compliance.

Loan Origination Systems ensure structured onboarding and policy compliance. Once a loan is disbursed, LOS platforms go dark. No visibility into what happens next in the field.

The Execution Gap

Field officers often track visits, attendance, and collections using registers or disconnected tools. This data is reconciled later. That creates a gap between what happens in the field and what gets reported.

As a result, MFIs manage outcomes without consistent visibility into execution.

Why MFIs Need an Integrated LMS, LOS, and Field Force Automation Model

Field Force Automation (FFA) is a mobile tool. Field officers use it to log visits, attendance, and collections on the spot, not hours later.

An integrated model assigns a clear role to each layer:

LOS – Structured Onboarding

Borrower profiles, group structures, and loan terms are logged at the start.

LMS – Repayment and Portfolio Management

Schedules, dues, collections history, and portfolio data stay in one place.

Field Force Automation – Execution at the Center Level

FFA acts as the execution layer. It captures:

- Verified customer visits

- Attendance of borrowers and field officers

- Collections at the point of interaction

- Time and location stamps for each activity

- Exceptions and remarks in real time

When FFA integrates with LMS and LOS, execution data flows directly into core systems. No delays. No manual reconciliation.

This creates a single operational view of visits, collections, and portfolio performance.

What Changes When Center Meetings and Visits Are Digitised

Digitising center meetings and customer visits shifts MFIs from assumption to observation.

Key changes include:

- Verified attendance instead of assumed presence

- Collections recorded during meetings, not reconstructed later

- Time-stamped and geo-validated visit and payment records

- Immediate visibility into meeting outcomes and exceptions

- Reduced dependence on end-of-day or end-of-week reconciliation

MFIs stop guessing. They see what happened while they can still act on it.

How Digitised Execution Improves Collections Discipline

When visits and collections are captured in real time:

- Repayment discipline becomes more consistent

- Missed or partial collections surface immediately

- Follow-ups become timely and data-driven

- Variations across branches and field teams reduce

Discipline shifts from manual enforcement to process-led execution, improving predictability across the organisation.

Impact on Risk, Compliance, and Portfolio Health

Risk starts at the center level. It shows up in portfolio reports much later.

- Digitised center meetings help MFIs:

- Identify early delinquency patterns

- Detect execution gaps before they escalate

- Reduce the risk of errors and irregularities in field collections

- Maintain stronger audit trails for internal and regulatory reviews

With verified execution data, portfolio risk becomes observable and manageable, not retrospective.

Digitisation Must Support Field Teams

Field adoption determines the success of any digitisation initiative.

Effective solutions are designed around field realities:

- Simple, guided workflows

- Offline capability for low-connectivity regions

- Minimal data entry during center meetings

- Alignment with existing meeting formats

What MFIs Should Evaluate Before Digitising Visits and Collections

Before implementation, MFIs should evaluate solutions on operational fit, not feature lists.

Key considerations include:

- Ease of use for field teams

- Reliability in offline environments

- Integration with existing LMS and LOS platforms

- Ability to scale across branches without added complexity

The objective is stronger execution control with fewer operational gaps.

Predictable Growth Starts at the Center Level

Predictable portfolios start with disciplined center meetings

Predictable growth in microfinance begins with predictable execution at the center level.

When customer visits and center meetings are digitised, MFIs stop inferring what happened and start observing it as it happens. This shift from assumption to verification strengthens discipline, reduces risk, and builds confidence in portfolio data.

MFIs that integrate LMS, LOS, and Field Force Automation through TrackoField are not just digitising operations. They are building the execution foundation that predictable, scalable growth requires.

Apoorva Raizada is the Content Marketing Manager at TrackoBit. With over a decade of experience across media, advertising, and B2B SaaS, she brings a sharp editorial mindset to technology-led business... Read More

Related Blog

How to Manage Field Employee Expenses Efficiently: 7 Proven Ways

How field expense management software helps businesses reduce fraud, speed up approvals, and control field spending better.

Effective Risk Management in NBFCs: Tools, Techniques & Best Practices

Learn how effective risk management in NBFCs helps reduce NPAs and maintain a strong portfolio.

What Are The Roles and Responsibilities of a Field Sales Representative?

Field sales reps help manage territories, build relationships, and collect market data. Know how digital tools can help provide better…

Leave Balance Adjustment: Now Live in TrackoField

Simplify HR operations with TrackoField’s Leave Balance Adjustment. Configure probation-based leave and correct balances at scale, without waiting on the…

Your inbox awaits a welcome email. Stay tuned for the latest blog updates & expert insights.

"While you're here, dive into some more reads or grab quick bites from our social platforms!"Stay Updated on tech, telematics and mobility. Don't miss out on the latest in the industry.